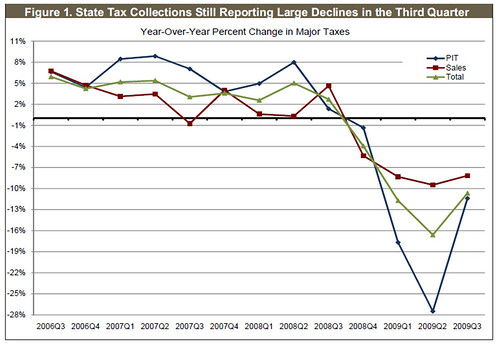

Fortunately, I have reassuring news for my Lenin-fearing compatriots: Not only is capitalism alive and well, but you are about to see it expand in ways that you could have never envisioned. Recently, the Census Bureau released its Survey of State Government Finances for 20098, in which they reported that state revenues were down 15.7% over 2007. Yesterday, Corina Eckl, the fiscal director of the the National Conference of State Legislators stated, "Even if the recession is over, state budgets are in appalling conditions and are going to be that way for quite a while. For many states, revenue recovery is not even in the forecast.” The Rockefeller Institute of Government gave similar results in its State Revenue Flash Report:

Clearly, the risk of municipal debt default is increasing quarterly. So far, the federal government has stepped in and made emergency loans to bridge gaps, so that unemployment benefits and welfare benefits can be paid. Everybody expects this to continue and I believe that everybody is wrong. While I'm certain that some federal aid will be given, the criteria for distribution will be based on nature of the bondholders are. If GS holds much of your city's debt, you might get a pass, but if it's pension and retirement funds, you'll probably be invited to go pound sand. But don't get too concerned, when things look bleakest, capitalism will save the day.

What I'm talking about is privatization on a unprecedented scale and implemented with as much subtlety as prison rape. John D. Rockefeller wasn't fooling when he said, "Competition is a sin." It is every capitalist's wettest dream to own a monopoly in a product with inelastic demand, like water, education, sanitary sewers, police and fire protection, and many other service provided by our current "socialist" model. We've already had a taste of this with the deregulation of certain electric companies. There is nothing new about this idea. As the following video describes, CH2M HILL has already successfully privatized two cities in Georgia; Sandy Springs and Johns Creek. However, both of these communities are well heeled and they both approached CH2M HILL voluntarily. Moreover, I imagine that CH2M HILL is on its best behavior due to the enormous potential for growth. Any community that gets a CH2M HILL or equivalent rammed down their throats due to an inability to obtain financing will likely be put through the ringer.