Tier 1 Capital: Tier 1 (core) capital includes: common equity plus noncumulative perpetual preferred stock plus minority interests in consolidated subsidiaries less goodwill and other ineligible intangible assets.

Risk-Weighted Assets: Assets that have been adjusted for potential default.(residential mortgage multiplier=0.5, commercial/industrial loan multiplier=1.0, cash and US treasuries=0.0, short-term credit,demand deposits=0.20)

1. Total Equity/Assets: Book value.

2. Texas Ratio=(Non-performing assets+REO)/(Equity-Intangibles-Goodwill+Loan Loss Reserves). Note that this is the only metric that accounts for non-performing assets.

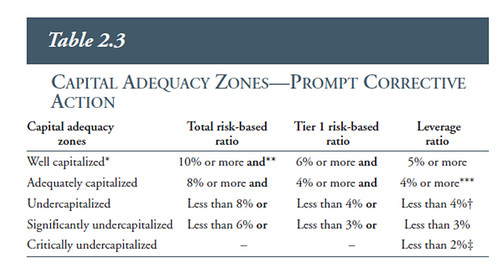

3. Leverage Ratio=(Tier1 Assets/Total Assets)

4. Tier 1 Risk Based Capital Ratio=(Tier 1 Capital)/(Risk Weighted Assets)

5. Total Risk Based Capital Ratio=(Total Risk Based Capital)/(Risk Weighted Assets)

MD Banks

Even a 'well capitalized' bank at 10% equity means leverage of 10 to 1.

ReplyDeletePrecisely and appears that the FDIC's risk based asset derating scheme could use some adjustment, since several of the recently failed banks appeared sufficiently capitalized in their last call report.

ReplyDelete