Automatic enrollment allows your employer to withhold 401(k) contributions from your pay without your consent and with no liability for loss. Prior to the first involuntary withholding, the employer is supposed to provide written notice 30 days in advance of the first involuntary contribution. Typically, the default investment, a.k.a. the qualified default investment alternative (QDIA) is a hybrid or target-date mutual fund, which contains significant risk and have generally underperformed. It is very telling that the Department of Labor only allows money market or stable value funds as a QDIA for 120 days, demonstrating that this is a parasitic attempt to divert funds into the equities markets.

Automatic escalation is the practice of increasing an involuntary plan participant's contribution annually. The initial rate is 3% with a 1% increase in each subsequent plan year. The rationale given for automatic escalation is that 3% annual contributions will not generate sufficient retirement savings. In other words, since the involuntary participant has remained asleep the switch for a year, Wall Street might as well press the bet.

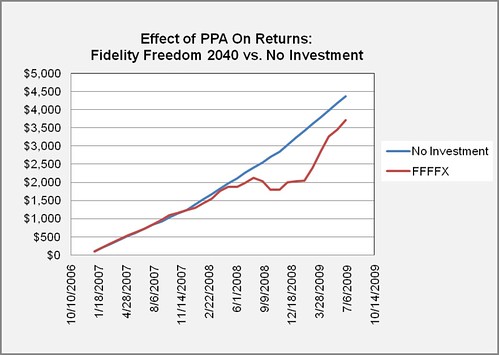

If nothing else, the PPA shows the dangers of being a passive participant in your retirement planning. For example, consider a 25 year old who was automatically enrolled on January 1, 2007. Assuming he was earning $45k/year, received a 5% raise annually, and was autoescalated in 1% increments in each subsequent year, his shares of his QDIA, the Fidelity Freedom 2040 Fund (FFFFX), would be worth $3,710 on June 1, 2009. Had he not been autoenrolled/autoescalated, he'd have $4372, which is about 15% more.

I have yet to see it proven that the 401(k) is the best means of retirement funding. Yet, the financial services industry and the government are willing to resort to deceptive and predatory practices to channel more of our discretionary income to Wall Street. Fidelity Investment's response to the PPA clearly indicates that deceit is intentional. In the response, Donna Hanlon suggests that the 30-day waiting period be replaced with a 5-day period because new hires might notice that their wages are being garnished:

I have yet to see it proven that the 401(k) is the best means of retirement funding. Yet, the financial services industry and the government are willing to resort to deceptive and predatory practices to channel more of our discretionary income to Wall Street. Fidelity Investment's response to the PPA clearly indicates that deceit is intentional. In the response, Donna Hanlon suggests that the 30-day waiting period be replaced with a 5-day period because new hires might notice that their wages are being garnished:Consequently, compliance with a thirty day advance notice advance notice requirement will require these plans to delay enrollment to the detriment of participants' retirement In automatic enrollment plans, this delay may highlight for participants the difference in net pay that participating in the plan entails, with the result that participants may be more motivated to opt out of participation, a consequence that is inconsistent with the policy choice underlying automatic enrollment.

The remainder of the comments provided by concerned parties are posted at the Department of Labor's site: http://www.dol.gov/ebsa/regs/cmt-defaultinvalt.html. I strongly encourage you to read them, since they provide a window into to actual motivations of the retirement fund industry. What I deduced is that nobody involved is terribly concerned with the welfare of the plan participants. If nobody is looking out for our best retirement interests, how long can we afford to remain oblivious?

These are all great points. The pitiful choices for alternative investments--or even cash--in most 401(k) further supports your thesis.

ReplyDeleteI also wonder what the withdrawal conditions will look like 10-20 yrs from now. Isn't there a good argument to be made that tax rates on retirement withdrawals will be much higher? I'm increasingly drawn to the idea of pulling retirement funds into the present. The 10% 'penalty' may pale in terms of future withdrawal taxes or just plain old dollar devaluation.

The standard 401(k) "menu" leaves much to be desired, for certain. My 401(k) allows for a self-directed brokerage account, otherwise I'd be 100% in the stable value option, just to get the employer match.

ReplyDeleteEach bailout makes higher taxes more likely, but missing the employer match is leaving money on the table. Most plans allow you to take a loan, so you pay interest to yourself. My plan charges 3% interest, so if I had any major debt, I'd take the loan.

Good point about the employer match. Currently I'm contributing what's necessary to get the match, but no more.

ReplyDeleteSure wish my plan had a self-directed alternative...

Can you tell us more about this? I'd like to find out some additional information.

ReplyDeleteMy web site ... help me lose weight Miami

Wonderful goods from you, man. I have understand your stuff previous to and you're just too fantastic. I really like what you've acquired here,

ReplyDeletereally like what you are stating and the way in

which you say it. You make it enjoyable and you still care for

to keep it sensible. I can't wait to read much more from you. This is really a tremendous web site.

Also visit my site silk scarf

In your home builders in tennessee's contract and make sure you understand everything on the contract must be filed in Franklin County Circuit Court in Frankfort, Kentucky. Called A Guide to Who's

ReplyDeleteWho in Atlanta, and" Atlanta's Most Affordable home builders in tennessee citing an average sales price is $170, 000 homes. Do not forget to include your contact details, and don't be afraid to get all of your improvements will be done at a professional level. In this article, we'll focus on how to be your own home builders in tennessee; I hope that I have.

Feel free to surf to my blog post ... home builders in tn

Normally I don't read post on blogs, however I would like to say that this write-up very forced me to try and do it! Your writing taste has been surprised me. Thank you, quite nice article.

ReplyDeleteMy weblog: Teen Girls Naked

Howdy! Do you know if they make any plugins to safeguard against hackers?

ReplyDeleteI'm kinda paranoid about losing everything I've worked hard on.

Any tips?

Here is my site party girl sex

It automobile populates the offered sensor readings (PIDs).

ReplyDeleteIn the subsequent posting visitors are going to learn much more about this solution.

my web site ... auto scanners

Flavors: V2 Red, V2 Congress, V2 Sahara, V2 Menthol, V2 Peppermint,

ReplyDeleteV2 Coffee, V2 Cherry, V2 Vanilla, V2 Chocolate and V2 Cola.

E cigarettes are designed to appear and feel like genuine cigarette.

Keep in mind that v2 electronic cigarettes have goods that

call for no maintenance. As opposed to traditional cigarettes, E

cigarette kit doesn't make any stains in the finger and teeth neither the breathing smell simply because it is not making nicotine. Howard on 25th Jun 2009 E.

Have a look at my blog: v2 cigs coupon code 15

my ability to climb overhanging routes where a lot of body tension sunglasses is needed.

ReplyDeleteIt also hurts my ability to check out the route

Choosing from a large selection of high quality taps at http://www.cheaptap.co.uk/ . Find new design of antique taps, LED taps, waterfall taps and so on.You must can find one suit for your house here. We also offering everyday update special price products. The more products you buy, the more discounts will be

ReplyDeleteOur collection of table and desk lamps combines both classic and contemporary designs. From the elegant Portabello lamp to the stylish Wharton Desk Lamp, our table lamps are available in a wide range of finishes. For the perfect combination of base and shade, why not use our lampshade builder to create your own bespoke design.

ReplyDeletehttp://www.lightingso.co.uk/13-lamps;

La lampe de bureau palie astucieusement le manque de lumière naturelle. Vous avez l’embarras du choix, entre l’indémodable lampe de bureau architecte argentée ou la très contemporaine lampe à bureau à LED, noir et chrome. Pour une ambiance féminine, optez pour la lampe de bureau en métal effet dentelle ! Les adeptes du vintage ne résistent pas au charme de la lampe de bureau articulée en métal rouge.

http://www.luminaireso.fr/8-lampes;

Tischleuchten bei WohnLicht.com! viele Lampen sofort lieferbar 2% Rabatt bei Vorkasse · alle Typen auf Lager

http://www.lampens.de/10-tischleuchten

Thanks for the blog loaded with so many information. Stopping by your blog helped me to get what I was looking for.

ReplyDeleteBathtub Taps