Speaking theoretically, because it seems to be impossible, if the American public grew a brain and realized that its representative republic had devolved into a corporate kleptocracy, how could they peacefully restore their sovereignty?

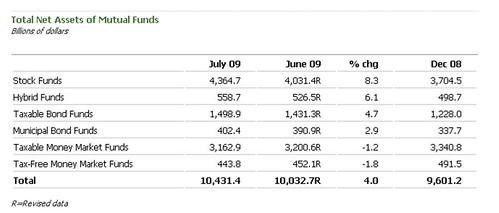

Forget about debtor's revolts, or coordinated bank runs. In both cases, I imagine that the Fed can print it faster than it could be removed. The answer is actually quite simple and pleasantly ironic: If the American people wish to reverse the usurpation of power by corporate entities, they should close their retirement savings accounts en masse. Why do I think this? According to the Wilshire Broad Markets Index, the total market capitalization for the NYSE, NASDAQ, and AMEX as of 8/31/09 is $12.04 trillion. Below you'll find The Investment Company Institute's latest mutual fund levels.

Note the $4.365 trillion in stock mutual funds and the $0.559 trillion in hybrid funds. If we conservatively assume the hybrid funds to be 50% invested in equities, the two sum to $4.644 trillion or 38% of the total stock market capitalization given by Wilshire. Mutual funds are primarily held by defined contribution plan participants (401k, 403b, etc), IRA participants, and retail investors seeking to augment their existing retirement plans, per the Investment Company Institute

Since we're talking about punching a permanent, $3-$5 trillion hole in the market, there would be resistance by Wall Street, fund management, and the US Government. However, the Fed and Treasury can't legally dump dollars into the equity markets like they can a bank.(Yes, I maintained a straight face while typing the previous sentence.) Fund operators would attempt to delay redemptions and use market circuit breakers to try to close the markets prematurely. As long as the dissenters were disciplined, such that every time that every time the market opened, a significant chunk of capitalization disappeared, I believe that the public could remind those in power precisely who it is that they work for.

Let me make this clear, I believe that Minch is sincere and should be commended for attempting to stand up to an out-of-control, predatory industry. Unfortunately, her plan is fatally flawed due to the Federal Reserve subsidized securitization of revolving credit via the TALF program. TALF is essentially the bastard child of Geithner's PPIP concept, where retail debt is securitized and the Federal Reserve Bank of NY makes low interest, non-recourse loans for near 90-95% of the face value of the securitization to interested buyers. The buyer then pledges the newly purchased and likely overvalued securities as collateral for the loan. TALF has been accepting credit card debt since May and has potentially put the taxpayer on the hook for around $20.1 billion. If any sort of organized default activity were to occur, the credit card companies would simply pile more debt into the TALF dumpster (The minimum loan amount is $10M and there is no maximum.) While I don't expect Ann Minch to know any of this, I find it difficult to believe that Smith is unaware of this. After all, she is an eminently qualified financial expert, just ask her:

Although I believe ideas should stand on their own merit, rather than on their author's credentials, I also recognize that readers want some assurance that they are not quoting a 13 year old or a dog. I have undergraduate and graduate degrees from Harvard. I have been working in and around the financial services industry since 1980 and have had over 40 articles published in venues such as The New York Times, Institutional Investor, The Daily Deal, U.S. Banker, Bank Mergers & Acquisitions, The Conference Board Magazine, BRW Magazine (Australia), and Boss Magazine (Australian Financial Review).

What Smith fails to mention in her bio is that she is also the President of Aurora Advisors, which is a financial management consulting firm serving Wall Street. Smith knows damn well that credit card lenders like JP Morgan Chase, Citigroup, and Bank of America (aka her potential and, perhaps, current clients) wouldn't be significantly impaired by Minch's debtor's revolt. The participants who would be harmed are the taxpayers, as usual, and the debtors. To be fair, Smith gives a half-assed warning about trashing your credit and statutes of limitations on the claims of creditors, but since she didn't look into the actual consequences to the debtor, it's fairly clear that's not where her sympathies lie.

In reality, if you walk away from a credit card debt, your account will go into collections after 30 days and your FICO score will be reduced dramatically. This may very will trigger drastic interest rate increases on your other cards. Eventually, the account will be sold at a deep discount to a collections agency that will harass you for payment for several months. Once they give up, they'll resort to legal means. You will be sued in civil court and if you fail to show up, a default judgement will be issued for the debt and the collector's legal fees and wage and asset garnishment will likely occur. If you insist on a trial, you won't have a leg to stand on, so the results will likely be the same, plus your legal fees. Don't underestimate the capacity of the civil courts, either. Every debt court that I've observed was a well-oiled machine in which default judgements were rendered at the pace of a standard auction.

Employers hate garnishment orders of any sort and view them as grounds for refusing employment. If you're already employed, they can't legally fire you for the garnishment resulting from a debt, but they can always manufacture another reason. In the video clip, Minch states that she is aware of the consequences, is judgement proof, and is willing to take the heat. From what I observed in the 4:28 minute clip, under no circumstances would I screw with Minch without the benefit of a concealed straight-razor and a good pair of track shoes. For the rest of us, this strategy probably makes sense only if you are planning on filing for bankruptcy and can pass the means test for debt discharge (Ch.7 vs Ch.13).

Is Smith hopelessly naive or is she shilling for the Man? I really don't know. Everybody is here for a reason (including myself) and I doubt it's bloggers who are punching Smith's meal ticket. In fact, in Smith's position, writing a blog critical of Wall Street would appear to be one of the dumber things she could do. Is it possible that the adoration of anonymous strangers is worth risking your livelihood for? Who knows? The take away here is that it hasn't gotten any wiser to allow others to critically think for you.

If you are fortunate enough to be employed, I encourage you to take a long look at your last paystub. While it may be less than it was a year ago, what you see is still noteworthy, as it likely represents the most compensation that you will receive for a very long time. Welcome to the New Normal.

I'm certain that you've heard that consumer spending is responsible for 70% of the US GDP, ad nauseam. This figure is mostly worthless, without delving into the components of the consumer spending and earning. Zero Hedge had an excellent post titled, A Detailed Look At The Stratified U.S. Consumer, in which the debt levels and consumption patterns of the social classes are examined in detail. What ZH determined was that upper 10% held a disproportionate amount of disposable income relative to the middle and lower classes, which is made abundantly clear by the following ZH graphic: Source: ZeroHedge Thus, it was determined that the richest 10% accounted for 42% of consumption, the middle class (40%-90% net worth) accounted for 48% of consumption and lower class (0-40% net worth) were only responsible for only 12% of consumer spending: Source: ZeroHedgeRelatively speaking, the spending of the upper, middle, and lower class is 3.5:4:1, respectively. Thus, from the perspective of Wall Street, the lower class has few redeeming qualities and in fact poses more of a liability, due to the fact that consumers are also workers. Since the lower class can't add substantially to the left side of the balance sheet, it stands to reason that their right side influence should be reduced. Obviously, this can be accomplished via outsourcing, but this is rarely as profitable as advertised, due to shipping and complications that arise from operating in the third world.

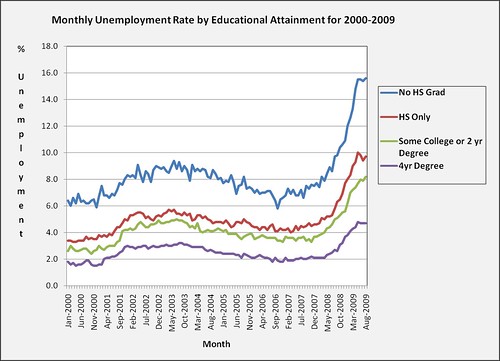

So, how can the third world be brought here? Immigration laws can go unenforced to maintain wage floors that are unlivable for legal workers. The threat of outsourcing and the reduction of workers' rights can be used to defeat any attempt at worker organization. All of this has been done flawlessly. Real wages in this country have stagnated over the last decade, regardless of what part of the boom/bust cycle we were in. However, the perfection of this scenario requires stratified, permanently high unemployment. If high unemployment can be maintained amongst the working class and moderate unemployment in the middle class, the employer take backs will be tremendous. Can it be done? I have every confidence:

Source: BLS, Datasets LNS14027659, LNS14027660, LNS14027689, and LNS14027662.

I may well be a 13 year old and/or a dog. I'm infinitely more interested in promoting critical thinking and evaluation, than credibility. The outsourcing of analysis to pundits, demagogues, and "experts" was no small contributor to our current situation.