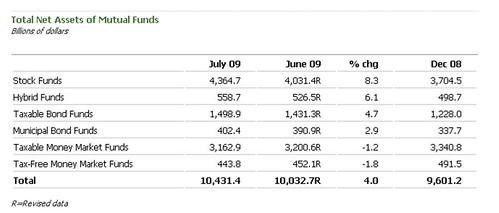

Forget about debtor's revolts, or coordinated bank runs. In both cases, I imagine that the Fed can print it faster than it could be removed. The answer is actually quite simple and pleasantly ironic: If the American people wish to reverse the usurpation of power by corporate entities, they should close their retirement savings accounts en masse. Why do I think this? According to the Wilshire Broad Markets Index, the total market capitalization for the NYSE, NASDAQ, and AMEX as of 8/31/09 is $12.04 trillion. Below you'll find The Investment Company Institute's latest mutual fund levels.

Note the $4.365 trillion in stock mutual funds and the $0.559 trillion in hybrid funds. If we conservatively assume the hybrid funds to be 50% invested in equities, the two sum to $4.644 trillion or 38% of the total stock market capitalization given by Wilshire. Mutual funds are primarily held by defined contribution plan participants (401k, 403b, etc), IRA participants, and retail investors seeking to augment their existing retirement plans, per the Investment Company Institute

Since we're talking about punching a permanent, $3-$5 trillion hole in the market, there would be resistance by Wall Street, fund management, and the US Government. However, the Fed and Treasury can't legally dump dollars into the equity markets like they can a bank.(Yes, I maintained a straight face while typing the previous sentence.) Fund operators would attempt to delay redemptions and use market circuit breakers to try to close the markets prematurely. As long as the dissenters were disciplined, such that every time that every time the market opened, a significant chunk of capitalization disappeared, I believe that the public could remind those in power precisely who it is that they work for.

This year I took an early withdrawal of some IRA funds. To me, the 10% penalty is trivial given future uncertainty re tax regs etc. It felt good to have those resources in hand today, rather than 'hoping' I'll have them down the road. I plan to continue this program in the future.

ReplyDeleteIn a DC account, the penalty is the 20% tax, plus a potential 10% penalty. I've drained 2 401(k)s and never got hit with the penalty. I still have a 401(k) w/ my current employer to get the match, but its a self-directed brokerage account through Fidelity. If I was restricted to Fidelity's cafeteria plan of bad mutual funds, I'd put 100% into the money market fund and sweep it annually. Even with the 20% penalty, I'd still be up 30%, due to the match.

ReplyDelete